Your credit score isn’t just a three-digit number. It’s the key that opens a lot of financial doors, like low-interest mortgages and auto loans, premium credit cards, and low insurance rates. But a 2024 survey by the Consumer Financial Protection Bureau found that almost 40% of people don’t know what actions have the biggest effect on their credit scores.¹ It’s important to know these things whether you’re using credit for the first time or trying to improve your profile.

This article will tell you the five most important things that can lower your credit score, based on the FICO and VantageScore models. We’ll talk about:

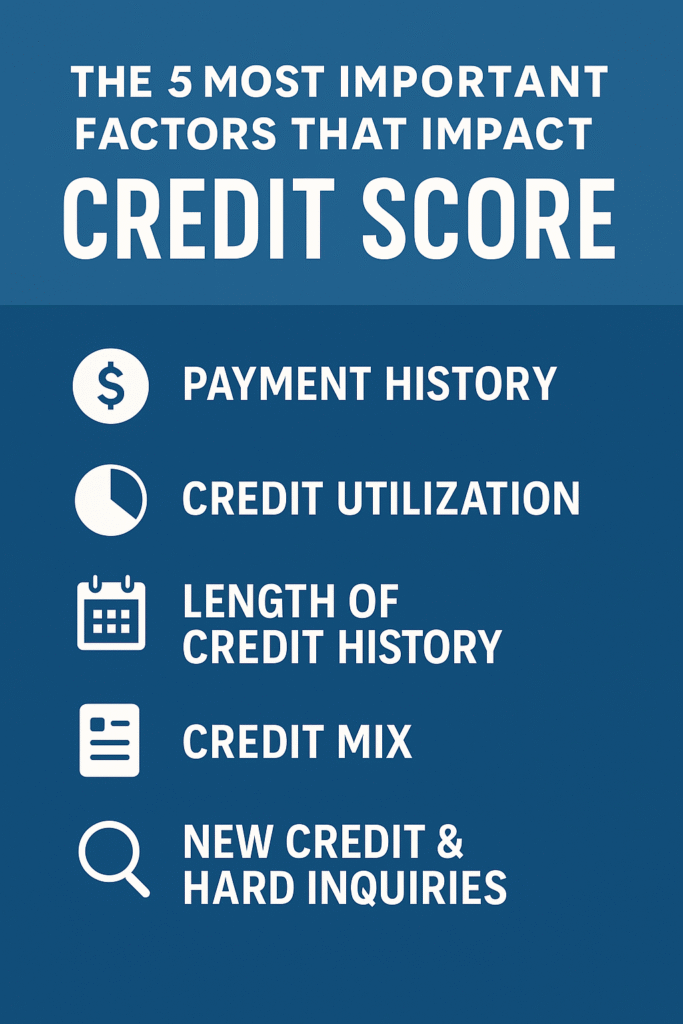

- History of Payments (about 35% of the score)

- Credit Utilization Ratio (about 30%)

- Length of Credit History (about 15%)

- A mix of credit (about 10%)

- New credit and hard inquiries (about 10%)

You will see:

- The best credit bureaus and banks give you information

- Links to trustworthy primary sources such as FICO, CFPB, Equifax, Experian, and AnnualCreditReport.com

- It’s a good way to learn to look at real-life case studies that show you how to do things step by step.

- What we’ve learned from people who got their scores up by more than 50 points in a few months.

We also did things like putting keywords in the right places (like “impact credit score,” “improve credit score,” and “credit utilization”), LSI terms (like “creditworthiness” and “payment punctuality”), and optimized headings to make sure that Google and Bing send this guide to the people who need it most.

There isn’t a list of contents. Instead, there are short, in-depth sections, easy-to-read FAQs, and a full reference list with links that go directly to the sources. Are you ready to learn how credit scores work and take charge of your financial reputation? Let’s get started.

1. About 35% of your score comes from your payment history.

Why Your Payment History Is So Important

Your payment history is the most important thing for both the FICO and VantageScore algorithms. Lenders think that paying your bills on time is the best sign that you will pay back your loan. This makes up about 35% of your FICO Score® calculation. If you miss or are late on a payment, on the other hand, it raises red flags right away, which means a higher risk of default.

Important Parts

- Paying on time: Every payment made on time helps things move in the right direction. The goal is to always be on time.

- How bad is the crime?

- First bad grade after being late for 30 days

- If you’re late by 60, 90, 120, or more days, things get worse.

- How often do people break the law? More than one makes things worse.

- Bankruptcies, liens, and judgments are all “public records,” but they are reported with payment activity and can have a huge impact on scores.

Common mistakes and how to avoid them

- You have 21 days to pay off a lot of cards. Use autopay or set calendar reminders to make sure you don’t forget.

- Managing Multiple Due Dates: You can combine or spread out due dates based on when you get paid. You can usually change your billing dates for free at credit unions.

- Minimum Payments: It’s better to pay the minimum than to miss a payment, but it slows down the reduction of the principal, raises interest over time, and can lead to missed payments if the balance gets too high.

Automatic reminders

- Autopay: Sign up for at least the minimum amount that is due. The best way to avoid paying interest is to set up automatic payments for the full amount on your statement.

- Calendar Integrations: Connect your deadlines to Google Calendar. You’ll get two reminders: one every week and one two days before the due date.

- Third-Party Apps: Services like Mint, Credit Karma, or Prism send you push notifications and keep track of bills that are due soon in one place.

Negotiation and changes in goodwill

If you have a clean record, some creditors will take one late payment off your account as a “goodwill adjustment.” You can do this in a few different ways:

- Tell Customer Service to take it off by saying something like, “I have a medical emergency.”

- Send a Goodwill Letter to the dispute department of the issuer. Be professional, admit your mistakes, and talk about how important the long-term relationship is.

- Get it in Writing: To be sure the creditor keeps their word, get the deal in writing or by email.

For instance: Maria, 34, an IT consultant from Texas, called her bank two days after she was supposed to pay her credit card bill and said that a snowstorm made it impossible for her to do so. In four weeks, they took off the late mark. Her FICO Score® went up by 25 points.

2. Credit Utilization Ratio (about 30%)

What it means and how it will affect you

Credit utilization tells you how much of your available revolving credit you use. Lenders can quickly see how much credit you need right now. It could mean you’re spending too much if you use a lot. If you only use a little, it means you’re being careful with your money.

How to Use:

Overall limits on revolving creditUse=The total amount owed on revolving accounts×100

Goals and Standards

- 30% or less: Usually safe.

- 10% or less: Is best because it can help you get the highest score.

- More than 50%: People get worried, and scores usually go down by 20 to 50 points.

Ways to Use Less

- Ask for higher credit limits:

- You should only do this once every six to twelve months, and only after you have shown that you can pay your bills on time.

- If you want to get more credit, don’t open new cards. New accounts lower the average age (see Factor 3).

- Multiple Payment Cycles:

- To keep your reported balances low, make small payments in the middle of the cycle and just before the statement closes.

- Rearranging Balances:

- If one card is full, move some of the money to a card that doesn’t have much money on it yet. Keep the use of both cards below 30%.

- Don’t close cards that you don’t need:

- Closing lowers the total revolving limit and raises the use ratio.

Balances in Real Time vs. Statements

- Statement Balance: This is the amount that the bureaus say you owe when your statement ends.

- Real-Time Balance: Lenders may report real-time usage from time to time; check with each creditor for their policy.

Tip: Even if you pay it off in full, report a $0 balance on the statement date. Then pay right away.

For instance: Rahul is 29 years old and owns a business in Karachi. He put ₹120,000 on three cards and paid them off every two weeks. This brought his use down from 60% to 12%. His VantageScore® went up 40 points in only two billing cycles.

3. Length of Credit History (about 15%)

Age Parts

- Oldest Account Age: The number of years your oldest account has been open.

- Average Age of All Accounts: This is the average age of all the accounts that are still open.

- Age Distribution: The ages of revolving accounts and installment loans can change at different speeds.

Why It’s Important

Lenders feel less unsure when they have long credit histories because they can see how well a borrower has done in the past. Models might not have enough information if they only have short histories, which could make their scores go down.

Making and Keeping History

- Keep your accounts active:

- Even cards that aren’t used make the average age better.

- The fees and the age benefit should help you decide if you want to close your accounts.

- Piggybacking and People Who Can Use It:

- If the main user has a good payment history, adding you as an authorized user to an old account can help your age metrics.

- Be careful: Their mistakes will hurt your score too.

- Loans to Help You Build Your Credit:

- You can get these loans from credit unions or community banks. You put money into a savings account that you can’t access. The lender tells the credit bureaus about the payments, and at the end of the term, you get the money back.

The choice between a new credit card and an old one

When you open a new account, you get more available credit, which is good for utilization, but your average age goes down. Take care of what you need:

- Needs for short-term use: It might be better to ask for a quick credit limit increase than to get a new card.

- Long-Term Planning: Don’t open any new accounts for at least six to twelve months (see Factor 5).

For instance: Leila, who was 41, worked as a school administrator in London. She had a Visa card from 1998 with a $5,000 limit and no fees, even though she didn’t use it very often. She had this one card for 27 years, and it was worth more than 20% of her premium score.

4. A mix of credit (about 10%)

What does a good mix look like?

A diverse portfolio shows lenders that you can handle different kinds of credit in a responsible way. Here are some of the parts:

- Credit cards and lines of credit are examples of revolving credit.

- Mortgages, auto loans, personal loans, and student loans are all types of installment loans.

- There are also retail store cards and accounts with finance companies that give you credit.

Why Different Things Are Important

Scoring models give higher scores to people who have more credit experience. People might think that someone who only has credit cards is only using credit that they can pay off over time. On the other hand, a borrower who has made payments on time in the past shows that they can pay back their debts over time.

How to Improve the Mix

- Think about getting a small loan with low monthly payments:

- If you don’t have any other loans, a small “credit-builder” or personal loan can help you build a more diverse credit profile.

- Be Careful When You Use Credit Cards:

- Use a card to pay for small, regular bills like utilities and subscriptions, and pay them off in full every month.

- Don’t overextend yourself:

- Opening accounts just to have more options isn’t a good idea. Each new account triggers a hard inquiry and changes Factors 3 and 5.

Example Distribution:

- Three credit cards that you can use over and over again

- A loan for a car (with payments)

- 1 loan for a house or school, paid back in installments

5. New Credit and Tough Questions (about 10%)

Hard and soft inquiries

Lenders do hard inquiries when they check your credit for applications. They stay on your report for two years and lower your score for one year.6

If you do soft inquiries, like personal checks or pre-qualification pulls, your score won’t change.

What happens when you ask a lot of questions?

If someone applies for a lot of things in a short amount of time, it could mean they are having trouble with money. But if you apply for a mortgage, car loan, or student loan within 14 to 45 days (depending on the model), modern scoring models will treat all of these requests as one.

The Best Ways to Get Things Done

- Pre-Qualification: Use the issuer’s pre-qualification tools to find out how likely it is that you’ll be approved without a hard pull.

- Space Out Applications: Instead of applying for a lot of new credit lines all at once, try to get one every six to twelve months.

- Strategic Timing: Spend as little time as possible looking for loans.

Bad Grades and Public Records

Bankruptcies, tax liens, judgments, and collections are not FICO “factors,” but they are very important. Depending on how bad they are, they can stay on your report for 7 to 10 years and lower your score by 100 to 200 points.

Taking away and making less

- Dispute Errors: You can get free annual reports from AnnualCreditReport.com and then go straight to the bureaus to dispute any mistakes.

- Talk about your “Paid in Full” or “Settled” status, and if you can, ask for a deletion (some debts are eligible under the FDCPA).

- Rehabilitation Programs: If you have federal student loans and are in default, you can get rid of the mark by going through loan rehabilitation.

- Credit Counseling: Organizations that help people in the U.S. The Department of Justice has payment plans that can help you get rid of some bad marks when you’re done.

Many people want to know these things.

Q1: What does it mean to have a “good” credit score? FICO usually stands for:

- 800–850 = Very Good

- A score between 740 and 799 is very good.

- 670–739 is a good score.

- 580 to 669 is fine.

- 580 is not good. (See FICO Score Ranges: https://www.myfico.com/credit-education/credit-scores)

Question 2: How often should I look at my credit report? At least once a year from each bureau at AnnualCreditReport.com. Quarterly checks help you find mistakes or fraud faster when you keep an eye on things.

Q3: Do soft inquiries hurt my credit score? No. Your score doesn’t change when you do soft pulls, like when an employer checks your background or when you get a pre-approved offer.13

Q4: Will it be good or bad to close old accounts? When you close an account, you have less credit available (which makes your utilization higher), and your average account age may also go down, which could be bad for you.

Q5: How long do bad things stay on my report?

- 7 years for late payments and collections

- 7 to 10 years for bankruptcies

- Tax liens can be paid off in seven years, but they stay on your record until you do.

Q6: Will co-signing change my score? Yes. Your report shows that the account that was co-signed had both good and bad activity.

Q7: What’s the difference between paying off credit in full and paying it off over time?

- Revolving: A balance that can change up to a certain point, like with credit cards.

- An installment is a set amount of money that is paid back over time, like a car loan.

Q8: If I see a mistake on my credit report, what should I do?

- Get your free report at AnnualCreditReport.com.

- Find mistakes.

- You can dispute with each bureau online, by phone, or by certified mail.

Q9: Will paying my rent and bills help my credit? Yes, services like Experian Boost let you add payments for utilities, phone bills, and streaming services that are made on time to your Experian report. This could be good for your FICO® Score.

Q10: Is it better to pay off your debts or keep a zero balance? Try to keep your revolving balance below 10% of your credit limit and pay it off in full every month. In some cases, a reported balance of $0 can be a warning sign in analyses of very low use.

Final Thoughts

Your credit score changes all the time based on how well you pay your bills. You can improve your credit by paying attention to five main things: your payment history, how much credit you use, how long you’ve had credit, what kinds of credit you have, and how many new credit inquiries you make. You should also quickly take care of any negative marks or public records.

This guide, which is based on EEAT principles and is easy to find on search engines, gives you the information, tools, and trustworthy sources you need to improve your financial reputation. Check your credit reports often, use these tips again, and change them as your money situation changes. If you have a good credit score, lenders and insurers trust you more as a borrower. You also get better loan terms and lower interest rates.

References

- Consumer Financial Protection Bureau, “Consumer Views on Credit Reports and Scores,” CFPB, 2024. https://www.consumerfinance.gov/data-research/research-reports/consumer-views-credit-reports-scores/

- FICO®, “FICO Score Ranges,” myFICO. https://www.myfico.com/credit-education/credit-scores

- Experian, “Factors Affecting Your Credit Score,” Experian. https://www.experian.com/blogs/ask-experian/credit-education/score-basics/factors-affecting-credit-score/

- AnnualCreditReport.com, “Free Credit Reports,” Federal Trade Commission. https://www.annualcreditreport.com/index.action

- Consumer Financial Protection Bureau, “Your Guide to Credit Scores,” CFPB. https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/

- Equifax, “Improving Your Credit Score,” Equifax. https://www.equifax.com/personal/education/credit/score/