It can be hard to take charge of your money, especially if you’re living paycheck to paycheck or trying to reach more than one goal at a time. But the first step toward being financially free is to have a clear, organized plan for where every rupee goes each month. This complete guide will teach you why budgeting is important, go into detail about five of the best and easiest-to-use budget templates, and show you how to pick the one that works best for you and stick with it. By the end, you’ll have everything you need to make a budget that works perfectly for your life.

1. Beginning

Have you ever looked at your bank statement and thought, “Where did all my money go?” You’re not the only one. A survey from 2024 found that almost 62% of adults say they worry about money more often than they would like, and almost half say they don’t know how they spend their money. That constant stress—worrying about bills that are coming due, costs that come up out of nowhere, or just not having enough—takes away mental energy that you could be using to enjoy life, follow your passions, or plan for your future.

The cure? Making a budget. Budgeting isn’t about not having things; it’s about giving yourself power. It helps you see things clearly so you can make smart choices, plan for the future, and stop worrying about your bank account. Here’s why it’s important to have a good budget:

- Clear and controlled finances. A budget shows you how much money you make and how much you spend, so you don’t have to worry about surprises. You can also sleep better at night when you know exactly how much money you make and spend.

- Getting things done. A budget helps you set priorities and make your dreams into real goals. For example, it can help you build an emergency fund, save for a down payment on a house, or pay off high-interest debt.

- Less stress. People who actively manage a budget report much less financial stress and better overall health, according to studies. The fear of “What if an emergency comes up?” goes away when you know you have a plan.

- Finding unnecessary spending. Keeping track of your spending can help you find subscriptions you never use, impulse buys that add up over time, or recurring fees that you could negotiate or get rid of.

But a lot of people who try to budget give up after a few weeks. Some common mistakes are:

- Feeling bored. It can feel like busywork to log every transaction by hand, especially if you don’t see any immediate benefits.

- Paralysis from too much analysis. There are so many ways and apps to choose from that it’s hard to know where to start, so people put off doing anything.

- Structures that don’t move. Templates that don’t take into account how income and expenses change in the real world can be frustrating because life doesn’t always go as planned.

That’s when budget templates come in handy. Pre-built frameworks make it easier to sort, assign, and keep track of things, so you can spend less time fighting with spreadsheets and more time making decisions. In this guide, we’ll go into:

- The top five budget templates, including what they are, their pros and cons, and how to use them, with real-life examples to help.

- Choosing the Right Template: questions for self-evaluation, ways to mix things up, and trial-and-error methods.

- Tips for Success—best practices for keeping and building momentum, including ideas from behavioral psychology.

- Questions and answers about common problems, like spending too much money or having income that isn’t steady.

By the time you’re done, you’ll be able to choose and use a budgeting system that works for you, whether you like cash, spreadsheets, or apps. Are you ready to change how you feel about money? Let’s get going.

2. The Core: 5 Best Budget Templates

2.1. The 50/30/20 Rule Budget Template

What It Is

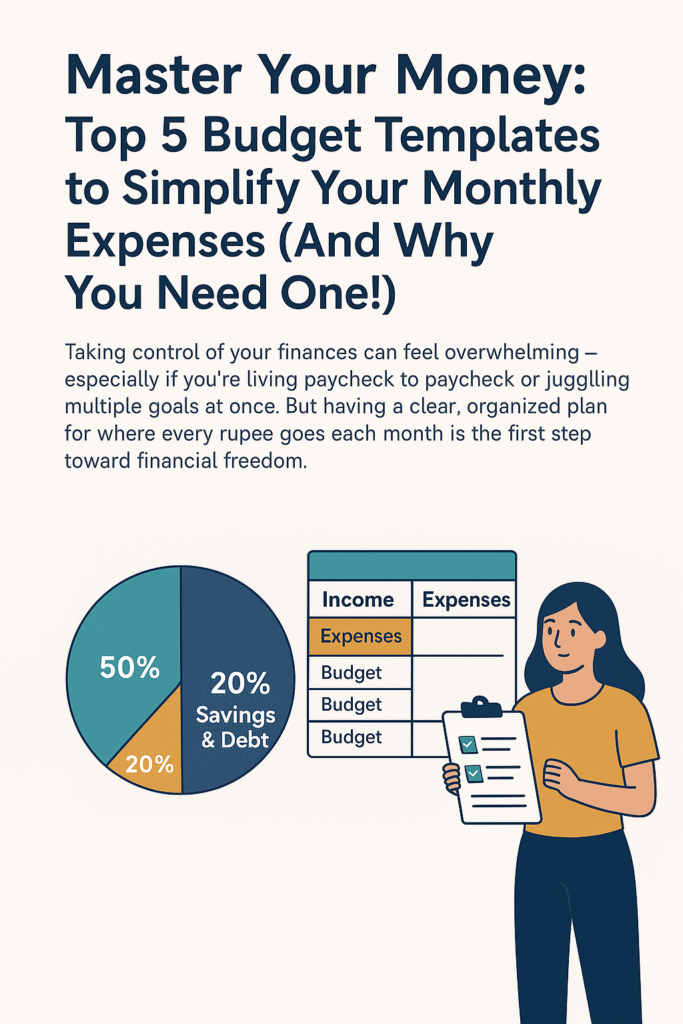

Senator Elizabeth Warren came up with the 50/30/20 Rule in her best-selling book All Your Worth: The Ultimate Lifetime Money Plan. It breaks down your after-tax income into three main groups:

- 50% Needs: Basic things like rent or mortgage, utilities, groceries, insurance, and minimum debt payments.

- 30% Wants: Things that aren’t necessary, like going out to eat, going to the movies, doing hobbies, traveling, and streaming services.

- 20% Savings and Debt Repayment: Putting money into emergency funds, investments, extra debt payments, and retirement accounts.

Why It Works

- Easy to use. You don’t have to keep track of a lot of small categories; you only have to keep track of three big ones. This makes it perfect for people who are new.

- Being able to change. You choose the subcategories and how they are split up within each bucket.

- Balance. Keeps you from saving too much and missing out on life or spending too much without building security.

Who Should Use It

- Beginners are scared of spreadsheets that are too detailed.

- People whose income is steady and whose costs are easy to predict.

- Anyone who wants to learn how to budget quickly.

Restrictions

- Not one size fits all; one size fits most. If your rent takes up 40% of your income, the “needs” bucket feels full.

- Households with a lot of debt or not enough money may need to set aside more than 20% of their income to pay off their debts.

- You need to be disciplined about your “wants.” It can be easy to let that 30% grow.

A Guide with Steps

- Add up all of your monthly income after taxes (for example, ₹100,000).

- To find out how much each bucket holds, multiply by 0.5, 0.3, and 0.2.

- Make a list of all your regular costs and put them into either Needs or Wants.

- Put the rest in Savings and Debt.

- Keep track of each purchase by using a simple spreadsheet or an app that lets you tag expenses by category.

- At the end of the month, check to see if you went over the “wants” limit. Can you save more money next month?

Example from real life

- Income after taxes: ₹120,000

- Needs (50%): ₹60,000

- Rent: ₹25,000

- Food: ₹10,000

- Utilities and the Internet: ₹5,000

- Insurance: ₹4,000

- Transportation: ₹6,000

- Minimum Payments on Loans: ₹10,000

- Wants (30%): ₹36,000

- Eating Out: ₹12,000

- Streaming and subscriptions: ₹4,000

- Gym membership and hobbies: ₹6,000

- Travel: ₹14,000

- Savings and Debt (20%): ₹24,000

- Fund for Emergencies: ₹10,000

- Extra Payment on Loan: ₹7,000

- Contribution to Retirement: ₹7,000

If Dining Out went up to ₹15,000 at the end of the month, you could cut ₹3,000 from Travel or cancel one subscription to stay within 30%.

Where to Look

- In Google Sheets or Excel, make three subtotal sections called Needs, Wants, and Savings. Then, use conditional formatting to highlight when you go over a bucket.

- Apps like Mint and PocketGuard let you categorize transactions as “needs,” “wants,” or “savings” and see how much money you have in each bucket in real time.

2.2. Template 2: A Budget with No Money (Zero-Based Budget)

What It Is

A zero-based budget “gives” every rupee you make a job. Your total income minus your expenses must equal zero. There is no money that isn’t being used; every rupee is put into a category, like a bill, a splurge, or a savings goal.

How It Works

- Most control possible. Plan out every rupee ahead of time so that you can’t spend money you don’t have.

- Stops money from being wasted. No “float” means that there won’t be any money in your checking account that you forgot about.

- Put your attention on your goals. You purposefully direct money toward important areas like an emergency fund, paying off debt, or investing.

Who It Works Best For

- Planners who pay attention to the little things and like to keep track of everything.

- People who work for themselves or on commission and have income that changes or is not steady.

- People who are determined to get rid of debt or save money quickly.

Limitations

- Takes a lot of time. To stay balanced, you may need to make changes every week or even every day.

- Not as flexible. If you’re strict, having to change your budget in the middle of the month because of an unexpected expense can be stressful.

- Keeping track of rigor. To keep things accurate, you need to write down every coffee, snack, and small expense.

A Guide with Steps

- Make a list of all the ways you made money this month, such as your job, freelance work, and side jobs.

- List all of your expenses, including fixed ones (like rent and insurance), variable ones (like groceries and utilities), and discretionary ones (like entertainment).

- Set aside a certain amount for each category until Total Income − Total Allocation = ₹0.

- Keep track of every transaction as it happens by using a spreadsheet or app to update your running balance.

- At the end of the month, reconcile. Any extra money will be carried over as a buffer for next month.

Example from real life

A conservative estimate of income is ₹90,000.

Distributions:

- Emergency Fund: ₹5,000

- Rent: ₹30,000

- Internet and utilities: ₹8,000

- Groceries: ₹12,000

- Transportation: ₹6,000

- Insurance: ₹4,000

- For fun: ₹5,000

- Eating Out: ₹6,000

- Other Buffer: ₹8,000

- Extra Debt Repayment: ₹8,000

- Account for Investment: ₹8,000

- Total: ₹90,000

If your real income reaches ₹100,000, you can split the extra ₹10,000 into three parts: ₹5,000 for a buffer, ₹3,000 for investments, and ₹2,000 for a one-time treat.

Where to Look for It

- Apps: YNAB (You Need A Budget) is the most popular zero-based tool. It helps you find a job for every dollar. Goodbudget has a digital version that works like an envelope.

- Spreadsheets: You can find free zero-based templates on personal finance blogs, or you can make your own by making rows for each category and making sure the “Remaining Balance” cell always says zero.

2.3. Template 3: The Envelope System

What It Is

The envelope system, which Dave Ramsey made famous, uses real or virtual envelopes with labels for different spending categories, like groceries, dining, fuel, and personal care. You put a certain amount of money in each envelope and only spend what’s inside.

Why It Works

- Limitations in the body. You can’t spend any more money when the envelope is empty. No overdrafts or surprise credit card bills.

- Tracking that you can see. When you handle cash, you are more aware of each purchase.

- Stops you from making impulse buys. The fact that you have to stop and get cash and then put it back makes you think before you spend.

Who Should Get It

- People who spend too much money without thinking.

- Households that only use cash or are teaching their kids how to budget.

- Anyone who can use tactile and visual cues to help them budget.

Limits

- Not useful for bills. You can’t use cash in an envelope to pay for rent, utilities, or subscriptions.

- Risk to security. You could lose or have your cash stolen, and carrying a lot of it is dangerous.

- Not easy. Taking money out of ATMs and sorting envelopes every pay period takes time.

A Guide with Steps

- Find out what kinds of things you’ll pay for with cash (like groceries, eating out, and transportation).

- Based on how much you’ve spent in the past, figure out how much cash you need in each envelope each month.

- Take out all the cash at the beginning of the month or pay period.

- Put money in labeled envelopes.

- Only use money from the right envelope. When it’s empty, that category is over.

- At the end of the month, count your leftovers and move any extra money to savings or roll it over into the next month.

Changes in Digital

Apps like Mvelopes, Goodbudget, and Qube Money work like the envelope system, connecting to your bank and following the same rules.

Example from real life

A young couple puts aside:

- Food: ₹15,000

- Eating out: ₹6,000

- Transportation and Fuel: ₹5,000

- Fun: ₹4,000

- Personal Care: ₹2,000

- Other: ₹3,000

They have ₹2,000 left over in Entertainment at the end of the month (which they put into savings), but they spend ₹1,000 too much on Dining Out. This means they have to borrow from the Miscellaneous envelope and eat out less next month.

Where to Look

- Physical Supplies: Get a set of strong envelopes or a wallet that organizes envelopes.

- Goodbudget and Mvelopes both have free tiers, but you can get more envelopes, rollover options, and syncing across devices by paying for premium features.

2.4. Template 4: Budget Spreadsheet Made Just for You

What It Is

A custom Excel or Google Sheets file where you can make everything, from categories and formulas to dashboards and charts. Think of it as your own personal financial control center.

Why It Works

- The most flexibility. Make exactly what you need—no extra fields, just your metrics and categories.

- Insights that you can see. Use charts and pivot tables together to quickly find trends, spikes, or places where you can do better.

- Able to grow. Start with the basics, then add more advanced features like tracking your net worth, your debt repayment schedule, or widgets that help you reach your goals.

Who Should Use It

- People who are good at math and know how to use spreadsheets.

- People who love data and like to change formulas, use charts, and change layouts.

- Tech-savvy people who want to be able to fully control their budgeting tool.

Limitations

- A steep learning curve. You need to know how to use formulas like

SUMIF,VLOOKUP,INDEX/MATCH, charts, and conditional formatting to use advanced features. - Entering by hand. You need to log every transaction, or your reports might not be correct.

- Extra costs for maintenance. If you add or delete rows or rename sheets the wrong way, formulas can break.

How to Do It Step by Step

- Transactions Tab: Make columns for Date, Description, Category, Amount, Payment Method (Credit/Debit/Cash), and Notes.

- Categories List: On a different tab, you can name your categories and put them in “Needs,” “Wants,” or “Savings” if you want a 50/30/20 view.

- Use

SUMIFSon the Summary Tab to add up amounts by category and month. - Dashboard:

- Pie chart showing the breakdown by category.

- Line chart for spending from month to month.

- A bar chart that shows the difference between what was planned and what actually happened in each category.

- Use conditional formatting to make categories that are over budget stand out in red.

Tips for Automating:

- Using named ranges makes it easier to keep track of formulas.

- Protect the formula cells so that they can’t be changed by mistake.

- Make dropdown menus for entering categories to keep things the same.

Example from Real Life

An entrepreneur keeps track of:

- Monthly Income: ₹150,000 (Salary and Freelance Work)

- Categories: Rent, utilities, payroll, marketing, travel, meals, office supplies, savings, taxes, and other expenses.

Insights from the Dashboard:

- Graphed that meals went up by 25% in May, which led to the decision to stop providing lunches and bring meals from home.

- Found that 30% of the budget for office supplies was not used, which made it possible to use that money for a coworking membership.

- Added tabs for assets and liabilities to keep track of net worth every month, which grew by 10% every year.

Where to Look

- Vertex42, Smartsheet, and Tiller Money all offer free templates for starting spreadsheets.

- YouTube channels like Leila Gharani or ExcelIsFun have step-by-step lessons on how to make budgeting models.

- Reddit’s r/personalfinance and r/excel are great places to get help with problems and come up with new formula hacks.

2.5. Template 5: Budgeting with an App

What It Is

Apps for phones and the web that connect directly to your bank accounts, automatically import transactions, sort your spending, and give you information through dashboards and notifications. Their goal is to make budgeting as easy and automatic as possible.

Why It Works

- Automating. No need to log transactions by hand; they sync in real time.

- Dashboards that are easy to use. Charts, progress bars, and visual summaries make keeping track fun.

- Setting goals and getting alerts. You can stay on top of things with reminders for bills that are due, warnings about low balances, and custom savings goals.

- Features for safety. Your data is safe with bank-level encryption and multi-factor authentication.

Who It Works Best For

- People who work a lot and don’t like entering data by hand.

- People who are tech-savvy and want things to be easy and “set it and forget it.”

- People who get help from automated nudges and reminders.

Limitations

- Mistakes in categorization. You will need to go over and change the categories of transactions that were tagged wrong, especially at first.

- Concerns about privacy. You need to trust the provider’s security measures when you link bank accounts.

- Costs of subscriptions. You usually have to pay a monthly fee for premium features.

- Dependence on technology. Tracking can be temporarily stopped by outages or sync problems.

Common Choices and Features

- Mint (Intuit) is free with ads and connects to more than 20,000 banks.

- Simplifi by Quicken has a clean, modern interface and lets you track subscriptions with one tap.

- Rocket Money has a free basic version and a premium tier that adds automated subscription cancellations.

- You Need A Budget (YNAB) is based on zero-based budgeting and comes with educational materials.

A Guide in Steps

- Download and install the app you want from the App Store or Google Play.

- Connect your checking, savings, credit card, and loan accounts in a safe way.

- Every week, look over and sort through imported transactions.

- Set budget goals for big areas like food, bills, and entertainment.

- Turn on notifications for bill reminders, warnings about low balances, and weekly or monthly email summaries.

- Track your goals, like savings milestones or a debt payoff tracker.

An example from real life

A software engineer uses Simplifi to:

- Connect two salaried accounts, a PayPal account for freelancers, and three credit cards.

- Set a budget of ₹30,000 for “Food & Dining” and ₹12,000 for “Transport & Fuel.”

- Get an alert when she reaches 75% of her food budget.

- Check the “Upcoming Bills” calendar to avoid late fees.

- Watch the “Watchlist” for subscriptions she no longer needs, saving ₹500 a month.

3. How to Pick the Best Budget Template for You

Everyone is different, and so should their budgets be. To find the right fit for you, ask yourself:

- What are the most important financial goals for me?

- If paying off debt is your top priority, zero-based might be best. If living a balanced life is more important, 50/30/20 might be best.

- How good am I with technology?

- If you like to have real controls, physical envelopes might be better. If you’re a digital native, you might prefer apps.

- What kind of person am I?

- Big-picture thinkers often do well with big buckets (50/30/20).

- Planners who pay attention to the details like granular zero-based or custom spreadsheet setups.

- How steady is my income?

- For regular salaried workers, 50/30/20 or apps are great.

- Zero-based or envelope systems are good for people who don’t earn money regularly.

- How much time can I give?

- Apps save time by doing things automatically.

- Spreadsheets or envelope systems need more work each week but can give you more information.

Trial and Error Is Important

Try each template out for a fair amount of time, like one to two months, and see which one you like best.

- Month 1: Try the 50/30/20 Rule with Mint or a simple sheet.

- Month 2: Switch to a zero-based template in YNAB or a free spreadsheet.

- Month 3: Try using envelopes for non-essential spending.

Pay attention to which method you dread the least and which gives you the clearest ideas. You can mix and match methods.

Important Point: The “best” budget template is the one that you will use all the time. It’s not perfection that moves the needle; it’s consistency.

4. How to Make Your Budget Work

It’s not just about the numbers when it comes to budgeting. Here are some tried-and-true ways to start and keep the habit:

- Be honest. Setting goals that are too high can make you burn out. If ₹5,000 a month for eating out seems too tight, start with ₹7,000 and cut back over a few months.

- Keep track of everything. Little costs add up. If you keep track of your daily ₹50 chai, you’ll quickly see that you’re spending ₹1,500 a month on it.

- Set up regular reviews. Set aside “budget dates” on your calendar for short weekly check-ins (15 minutes) and a longer monthly audit (30–60 minutes).

- Make the boring things automatic.

- Make saving automatic. Set up an automatic transfer to your emergency fund the day after each payday.

- Set up automatic payments for bills to avoid late fees.

- Change as you go. Life changes. Think of your budget as a living document that needs to be changed.

- Find your “why.” Link your budget to an emotional goal, like your child’s education, a dream trip, or peace of mind.

- Use tricks to change behavior.

- Visual cues: Print out your budget dashboard and put it somewhere you can see it.

- Reward systems: Get little treats for reaching your weekly goals.

- Accountability partners: Tell your spouse or friend about your goals.

- Celebrate Small Successes. Did you spend ₹2,000 less than you planned on eating out? Treat yourself to a little something nice without feeling bad about it.

5. Questions that are often asked (FAQs)

- Q1: What happens if I spend too much in a category? A: Don’t worry! First, figure out if it was a one-time thing or a pattern. If it happens again, move money around by cutting back on “wants” or changing the limits for next month.

- Q2: How often should I change my budget? A: Try to keep track of your expenses every day or at least once a week. At the end of the month, do a full audit.

- Q3: Is budgeting only for people who are having money problems? A: No way! Budgeting is a way for anyone who wants to be clear and in charge of their money to do so.

- Q4: What’s the difference between a financial plan and a budget? A: A budget helps you keep track of your short-term income and expenses. A financial plan lays out your long-term goals, such as retirement and investments.

- Q5: Is it possible to use more than one budgeting method? A: Yes, of course. Hybrid methods often combine the best parts of both systems.

- Q6: When will I see results? A: You’ll get immediate clarity. It usually takes 3 to 6 months of sticking to a budget to see real progress.

- Q7: What if my income isn’t steady? A: Use a zero-based or envelope system based on the month you think will be your lowest. Make a “Lean Month Fund” and fill it up during good months.

6. End

Budgeting isn’t about strict deprivation; it’s about giving you options and power. You decide where each rupee goes: to necessities, experiences, or making a safe future. You can choose the budget template that works best for you by looking at these five tried-and-true options.

What you should do next:

- Choose your template today: 50/30/20, zero-based, envelopes, a custom spreadsheet, or an app.

- Spend 30 to 60 minutes getting it ready.

- Make a promise to be consistent: set up weekly check-ins and a monthly audit.

Keep in mind that consistency is more important than perfection. Even if your budgeting habits aren’t perfect, they’ll get you closer to financial freedom than plans that you never follow. So don’t let another month go by without being clear. Pick your template, go through the process, and enjoy the peace of mind that comes with being in control of your money.

What ways of making a budget have worked for you? Please leave your tips and stories in the comments below!