It may seem hard to make a budget, but simple rules like the 50/30/20 rule have shown time and again that they can change your money situation. This rule basically splits your after-tax income into three clear groups:

- 50% for Needs: This is for things you need, like rent, groceries, utilities, and insurance.

- 30% for Wants: Things that aren’t necessary, like going out to eat, going to the movies, subscriptions, and hobbies.

- 20% for Savings or Paying Off Debt: This part is for setting up an emergency fund, saving for retirement, or paying off debts faster.

Even though it’s easy to follow, a lot of people still have trouble with it. Even the best budget plan can seem impossible when you have to deal with bills, unexpected costs, and lifestyle temptations. That’s why hearing real-life stories from people who were once in your shoes and were able to make amazing changes to their finances by following the 50/30/20 rule is so inspiring.

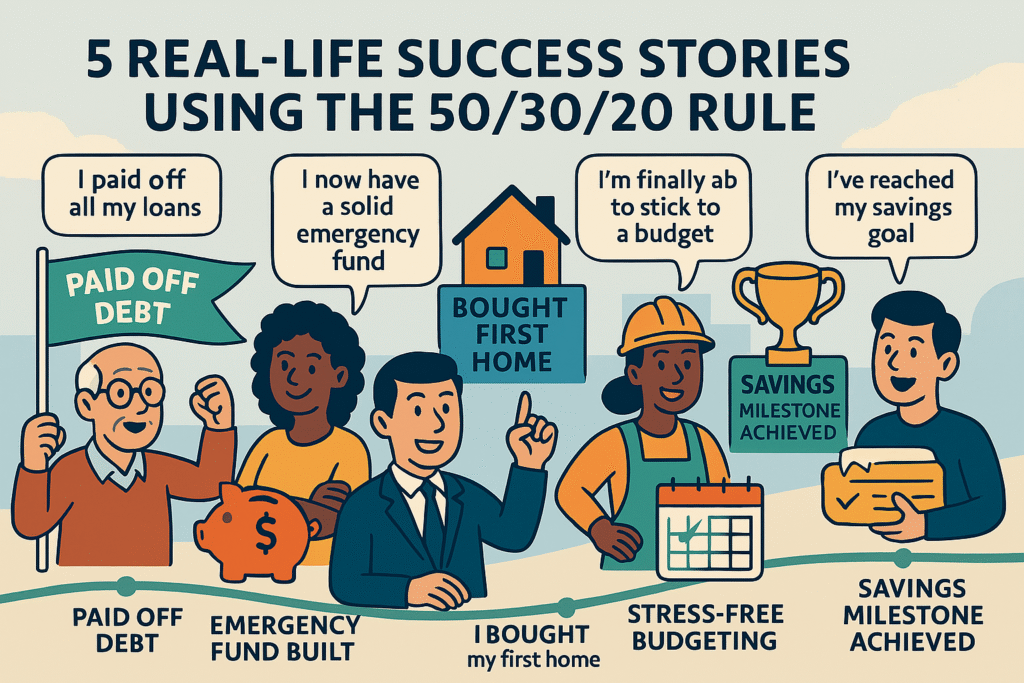

We tell five detailed success stories of people and families who used the 50/30/20 plan to get their finances back on track in this article. These stories are about people in different situations, like young professionals who are in a lot of credit card debt and retirees who are getting used to living on a fixed income. As you read each story, you’ll learn about the real steps they took, the problems they faced, and the amazing results they got. These real-life examples show that the 50/30/20 rule can change your life if you’re willing to be patient, disciplined, and flexible. You can use it to pay off debt, build a solid emergency fund, save for a house, or just lower your financial stress.

If you’ve ever thought that a simple way to budget couldn’t help you make money in the long run, let these stories put your mind at ease: real people with real problems have used this rule to not only get their finances back on track, but also to set themselves up for long-term success. Let’s take a look at these inspiring stories and see how you can start your own budgeting journey with more confidence.

A Quick Look at the 50/30/20 Rule

Before we look at our success stories, it’s important to know what the 50/30/20 budgeting plan is and why so many people use it. Here’s a quick summary:

- 50% for Needs: Needs are the things you need to live, like rent, utilities, groceries, transportation, insurance, and any other bills that come up every month. These are costs that you can’t change that are necessary for your health and survival.

- 30% for Things You Want: Wants are things you would like to have but could live without if you had to. This group could include things like going out to eat, monthly payments for things like streaming services or gym memberships, entertainment, travel, and other costs of living. This category is very important because it lets you have fun without feeling deprived, while also keeping your discretionary spending in check.

- 20% for paying off debt and saving: The last piece is for your future. This includes putting money aside for emergencies, retirement, investing, or making extra payments on debt. You can’t change this part—by automatically setting aside a certain amount, you steadily build financial security.

Why This Framework Is Effective:

- Clarity and Simplicity: By only having three broad categories, you don’t have to keep track of every single expense in great detail.

- Flexibility: The rule isn’t set in stone. A lot of people find that they can change parts of the rule when their lives change, like using a slightly different ratio in areas with high costs or during times of change.

- Responsibility: Keeping track of where every dollar goes helps you stick to your spending plan. It’s easier to stick to your budget when you can clearly see the differences between necessities, fun, and savings.

The 50/30/20 rule breaks your income into these separate parts, which gives you a clear path to financial stability while still allowing for the little things in life. When people consistently follow these rules, that’s when the real magic happens. The five success stories below are strong evidence that it works.

The first success story is about a young professional who paid off their credit card debt.

Meet Emily. She is 26 years old and just graduated from college. She started working with high hopes, but she quickly ran up $15,000 in credit card debt. At first, she lived a crazy life full of expensive gadgets, social events, and meals out. She didn’t have a set plan like a lot of young professionals do. Money went easily into her “wants” category, leaving little for savings and, even worse, adding up high-interest credit card debt.

The Problem

Emily’s budget was completely out of whack before she learned about the 50/30/20 rule. Her “wants” grew to almost 40% of her income, and she could barely afford the things she needed. The high interest rates on her credit card debt not only hurt her credit score, but they also made it hard to see a future without debt.

The Change

Emily knew that if she kept going the way she was, she would be stuck in a cycle of debt forever. She decided to try the 50/30/20 method after reading how easy it is. She was determined to change, so she:

- Looked over her bills again: Emily carefully sorted through every penny and found and reclassified expenses that she had wrongly thought were needs.

- Cut back on unnecessary spending: She cut her discretionary spending from 40% to the ideal 30% by choosing to eat at home and have fun for free instead of going out to eat and spend money.

- Used extra money to pay off debt: Emily put more money toward paying off her credit card balances after saving money by cutting back on things she didn’t need.

What She Did

- Made a detailed budget: Emily made a simple spreadsheet to show her income and expenses. She had a plan to follow because she clearly marked 50% of her net income for necessities, 30% for fun, and 20% for savings and debt.

- Used budgeting apps: To keep from going back to her old ways, she started using an app that showed her how much she was spending in real time. This made her honest about where her money was going.

- Set realistic goals: Emily didn’t try to pay off all her debt in one night. Instead, she set smaller goals, like paying off $3,000 in six months.

Problems and victories

It wasn’t easy to get used to this new discipline. Emily was always tempted by friends going out, online sales, and bills that came up out of the blue. But she stayed focused on her long-term goals and the freedom that would come from being debt-free. The results were amazing over the course of 18 months:

- Debt Gone: Emily paid off her $15,000 credit card debt in full.

- Better Credit Score: Her credit score went up a lot because she paid her bills on time and paid off her debt.

- Emergency Fund Set Up: She was able to set up a small emergency fund that would help her pay for unexpected costs.

Things You Can Learn from Emily’s Story

- Change the way you think about your spending: Small, optional costs can add up. You can free up money to pay off debt by giving them the right tasks.

- Set Small Goals: If you break a big problem down into smaller steps, it can help you stay motivated.

- Use Technology to Stay on Track: A good budgeting app or spreadsheet can help you remember to stick to your plan.

Tip to Remember:

If you have a lot of debt, you might want to lower the percentage of “wants” you have. Every dollar you save can help you get to financial freedom faster.

Success Story #2: A single parent making an emergency fund

Carlos was a single father with two young children. He was having a hard time because his income was inconsistent and his costs were going up. He often had to live paycheck to paycheck because of the unpredictable nature of his freelance work and the steady costs of childcare. He was very worried because he knew that without an emergency fund, one unexpected bill could throw his whole family into chaos.

The Problem

Carlos’s situation was made worse by the fact that freelance work is unpredictable. His income changed from month to month, which made it hard to stick to a strict budget. Also, the cost of good childcare and unexpected bills, like school supplies and small home repairs, meant that even his basic needs could sometimes go over the ideal 50% allocation.

The Turning Point

Carlos changed the 50/30/20 rule to fit with the ups and downs of his income after he realized he needed a financial cushion to protect his family’s future.

- Being able to change things was important. When his income was lower, he temporarily changed his allocation to put more money toward essential expenses and less toward savings.

- Tools for keeping track: Carlos started using a simple budgeting app that let him enter his income as it came in and change the categories for his spending.

- Automated savings: He set up automatic transfers to a special emergency fund whenever his income went up, making sure that the extra money never went to things that weren’t necessary.

What He Did

- Monthly Changes: Carlos learned how to budget by averaging his income over a few months. This gave him a good idea of how much he could spend.

- Needs and savings came first: He knew his income could change a lot, so he made sure that even in tight months, a little bit went to the emergency fund.

- Used Sinking Funds: He set up sinking funds for regular but unexpected costs, like yearly school fees, so that he could spread these costs out over the year.

Things that got in the way and things that went well

There were some problems along the way. Some months, the freelance work was so low that he had to make extra sacrifices just to meet his basic needs. There were times when unexpected costs almost stopped him from reaching his goals. But Carlos slowly built a sense of financial security by sticking to his new plan and keeping his eyes on the long-term goal. In a year:

- The emergency fund reached $5,000, which was a big deal that gave me peace of mind during times of financial uncertainty.

- Less financial stress: With a buffer in place, Carlos was better able to deal with unexpected costs without having to use high-interest credit.

- Better cash flow management: By keeping track of every dollar, he could better plan for and expect expenses.

Things You Can Learn from Carlos’s Story

- Being able to change is important: Life is full of surprises, especially when you don’t have a steady income. You need to be able to change your budget plan.

- Automation Helps: Setting up automatic transfers, even small ones, makes sure that saving isn’t left to chance.

- Keep track of every dollar: A budgeting tool can help you get a better idea of where your money goes by keeping track of your spending.

Tip to Take Away:

If your income is unpredictable, you should focus on building a buffer, even if it means changing your percentages for a short time. Keeping track of your money and making small, regular contributions to an emergency fund can change how stable your finances are.

Success Story #3: A couple saving up for a down payment on a house

Sarah and Marcus are a young couple with big dreams. They wanted to buy their first home within three years. They had a net income that let them spend some of it as they pleased, but they knew that without a clear plan, their dream of owning a home might slip away as their joint debt and daily costs kept rising.

The Problem

Sarah and Marcus, like many other couples, lived a comfortable life. But they spent more than 30% of their net income on “wants,” which is more than what is ideal. It was clear what they had to do: cut back on their spending and put more money toward a down payment while still having fun together on a smaller scale.

The Turning Point

They were determined to change their habits, so they decided to use the 50/30/20 rule:

- Rebalancing Priorities: They took a close look at their monthly expenses and saw that small changes, like cooking at home more often instead of going out to eat, could save them a lot of money.

- Automated Transfers: They set up automatic transfers into a special savings account for their home fund every payday.

- Joint Budgeting: They used a shared budgeting app to keep track of their spending and pool their resources, which made them more accountable and aware of their finances.

What They Did

- Monthly Budget Meetings: Sarah and Marcus started having “money talks” every week to go over their spending and make any necessary changes to their budgets.

- Cutting Unnecessary Costs: They stopped some subscriptions and limited shopping for things they didn’t need, bringing their “wants” down from 35% to about 30%.

- Setting Clear Goals: They set a realistic savings goal of $40,000 in three years and then worked backward to figure out how much they needed to save each month.

Problems and successes

The couple had to deal with problems that are common for anyone trying to reach a big financial goal:

- Temptations to Spend: Going to social events and making lifestyle changes were always hard. They stayed focused, though, by reminding themselves of their long-term goal.

- Unplanned Costs: Even with careful planning, there were times when unexpected costs came up. They decided to use a small buffer they had carefully set aside for times like this.

- Finding a balance between fun and discipline: They learned how to reward themselves without going overboard with their budget.

After three years of hard work:

- Saved $40,000 for a down payment: They were able to reach this important goal because they stuck to the 50/30/20 plan.

- Lowered Joint Debt: They were able to pay off extra debt quickly, which made them more trustworthy when it came to credit.

- Improved Relationship: Talking about their money issues together made their relationship stronger, which helped both their budget and their bond.

Things You Can Learn from Sarah and Marcus’s Story

- Teamwork is Strong: Working together on a budget can make everyone accountable and give them a common goal.

- Small Sacrifices Lead to Big Rewards: Making small changes to your lifestyle can save you a lot of money over time.

- Plan and Automate: Having clear goals and using automation can help you stay on track with your savings.

Tip to Remember:

If you’re saving for a big purchase like a house, use the 50/30/20 rule to put your long-term goals first. As a team, look over your budget often and celebrate each step you take toward your goal.

Success Story #4: A freelancer who can handle changing income

Meet Jordan: Jordan worked as a freelance graphic designer, and his income changed a lot from month to month. Some months, good contracts brought in extra money; other months, the income could drop a lot. This uncertainty made it hard for Jordan to stick to a budget, until he learned about the 50/30/20 rule.

The Problem

Jordan often had trouble planning ahead because his cash flow was not steady. When there was a lot of work, spending would go up, but when things were slow, even basic needs felt like a burden. The lack of a financial rhythm made it hard to make decisions. Sometimes they saved money by cutting corners, and other times they spent too much on luxuries when they were making a lot of money.

The Point of No Return

Jordan changed the 50/30/20 rule to fit his needs after realizing that he needed a structured way to get through the ups and downs.

- Finding an Average Income: Jordan started by keeping track of his income for six months to get a good idea of what a monthly average would be.

- Putting the Most Important Things First: In months with a lot of money, extra money went into savings. In months with less money, only the most important expenses were given priority.

- Using Technology: Jordan used budgeting apps and spreadsheet tools to automatically change allocations based on a running average and to separate irregular income from base earnings.

What was done

- Making a Buffer: A part of the money from high-earning months was always put into a “rainy day” fund, which kept the family’s finances stable during slow times.

- Monthly Income Reviews: Jordan went over the budget again every month to make better guesses and account for any extra money or losses.

- Clear Categorization: Jordan stayed within the 50/30/20 limits, which kept him from spending too much when things were going well.

Problems and Successes

It’s never easy to manage income that changes. Jordan faced a lot of problems:

- Overestimating Earnings: In some months, expectations were too high, which caused temporary overspending.

- Emotional Spending Spikes: There were times when a good month made people spend too much. Jordan was able to control these urges, though, by thinking about his long-term goals.

After a time of strict budgeting:

- Finances became more stable: Jordan’s cash flow became more predictable, and he developed a habit of saving that helped him get through lean months.

- Paid off student loans: The freelancer was able to pay off a lot of student debt by using extra money wisely.

- Started a Retirement Fund: Setting aside 20% of their income for savings led to the opening of a long-term investment account, which will help them become financially independent in the future.

What You Can Take Away from Jordan’s Story

- Being able to adapt is important: When your income changes, you need to be flexible but still stick to your plan.

- Track and Average: Use past data to make a budget that makes sense.

- Automate When You Can: Automation can help you spend less emotionally and keep your spending consistent even when your income changes.

Important Point:

Freelancers and gig workers can do well with the 50/30/20 rule if they figure out their average monthly income and set aside extra money during times when they make a lot of money to get through times when they don’t.

Success Story #5: A recent retiree is getting used to living on a fixed income.

Barbara is a retired woman who had a long and successful career. She now lives on a small fixed income from Social Security and a small pension. It was hard to go from a busy working life to a fixed income, especially since medical costs were going up and I had to make changes to my lifestyle. Barbara didn’t know how to change, so she used the 50/30/20 rule as a guide.

The Problem

Barbara had to rethink how she spent her money after she retired because her income dropped so suddenly. While things like healthcare and housing were still non-negotiable, they needed to cut back on luxury spending by a lot. Also, it was more important than ever to make sure she could keep a steady emergency fund, since unexpected medical bills could quickly throw her finances off balance.

The Point of No Return

Barbara adapted the 50/30/20 rule to fit her new life:

- Adjusted Ratios: Barbara changed the percentages a little bit with fixed income, giving “wants” a little less and “needs” and savings a little more.

- Focus on the Basics: By carefully reclassifying her expenses, she was able to find places where she could cut back, especially on things she didn’t need.

- Planning with Care: Barbara was able to see where every dollar was going by making a detailed monthly list of her expenses and using simple tracking tools.

Things that were done

- Detailed Expense Tracking: Barbara used to write down her expenses by hand in a special notebook, but then she switched to a free budgeting app made for retirees.

- Reassessing Priorities: She cut back on or got rid of unnecessary expenses, like going out to eat and subscriptions she didn’t need, and put that money into a healthcare contingency fund.

- Making a Stable Buffer: Because medical costs can be hard to predict, Barbara made a firm promise to save a part of her income each month for emergencies.

Problems and Successes

There were bumps along the way for Barbara:

- Getting rid of old spending habits: It was hard for her to stop doing things she had been doing for a long time that didn’t make sense in retirement.

- Getting used to a new pace: With a fixed income, every unexpected bill taught me how to budget better.

In the end, Barbara made a lot of progress:

- Living in Comfort: Changing her way of life let her pay for basic needs without worrying about them.

- Clear Spending Priorities: Barbara felt more in charge and less stressed about money when the rule was changed.

- Peace of Mind: She no longer had to worry about unexpected costs ruining her quality of life because she had a well-established emergency fund.

What Barbara’s Story Can Teach You

- Change the Rule to Fit Your Life Stage: When you retire, you may need to change the way you budget, but the main idea of balanced budgeting stays the same.

- Put What’s Important First: Cutting out unnecessary spending in favor of financial security can make a big difference.

- Embrace Simplicity: No matter if you use digital tools or write things down by hand, the most important thing is to be consistent.

Tip to remember:

If you have a fixed income, don’t be afraid to change the 50/30/20 percentages. Your goal is to feel safe and at peace. Always put the most important things and savings first.

Important Things to Remember from These Stories

There are a few common themes that come up in these powerful success stories that are very helpful for anyone thinking about or already using the 50/30/20 rule:

- Discipline and Consistency: Every success story shows how important it is to set clear goals and stick to them, even when you’re tempted or things don’t go as planned.

- Being able to change is important: Changing the base percentages to fit your needs is not a sign of failure, whether you work for yourself or are retired. It’s a smart move.

- Tools and technology for tracking: Using technology can turn vague budgeting ideas into daily habits that you can follow. For example, you can use budgeting apps or simple spreadsheets.

- Change of Mindset: Following the 50/30/20 rule can change the way you think about money in a big way. Instead of seeing budgeting as a chore, you can see it as a way to get real financial freedom.

- Support and Community: Using a community for accountability can make the journey less lonely and more rewarding, whether it’s through couples budgeting together or checking in on finances with friends on a regular basis.

The 50/30/20 method is not a one-size-fits-all formula; it is a flexible framework that works when it is changed to fit each person’s needs. The stories we’ve shared today show that you can take charge of your money and reach your goals, no matter how much money you make, how you live, or how you messed up your finances in the past.

The end

These real-life success stories show how the 50/30/20 budgeting rule can change your life. This simple framework can help you get your finances in order, whether you’re a young professional, a single parent, a couple dreaming of owning a home, a freelancer with an unpredictable income, or a retiree who needs to stick to a fixed monthly budget.

You can get a better handle on your money and take steps that will make a big difference in your finances by dividing your income into three easy-to-manage groups: 50% for needs, 30% for wants, and 20% for savings/debt. You can get through tough times, pay off debts, save for long-term goals like buying a home, and even build a safe emergency fund if you have the right attitude, make smart changes, and stay determined. The stories of Emily, Carlos, Sarah, Marcus, Jordan, and Barbara show this.

It’s not about becoming perfect overnight on the road to financial freedom; it’s about making small, thoughtful choices that add up over time. If these stories have motivated you, do something small today: look at how you spend your money, use the 50/30/20 rule, and be patient as you watch your finances change. The rule is strong, adaptable, and, most importantly, it has been proven to work. You can start your own budgeting success story today. Remember that every little change you make will help you stay financially stable for a long time.

Questions and Answers Section

Question 1. How long does it usually take to see results from the 50/30/20 rule?

Most people start to see changes in how they budget after using the same methods for three to six months. Real-life experiences show that real progress, like paying off debt or building up an emergency fund, often happens in 12 to 18 months. But even small positive changes can make you feel better about yourself right away.

Q2. Can the rule still work if I owe money and don’t have any savings?

Yes, for sure. The 50/30/20 framework is actually meant to help you pay off debt while also saving money. It encourages you to set aside money on purpose to pay off debt and build an emergency fund. A lot of success stories are about people who started out with a lot of debt and then followed this rule to become financially stable over time.

Q3. What if I want more than 30% of my net income all the time?

A lot of people have this problem. The most important thing is to be honest about how you categorize your expenses and cut back on things you don’t need. Use tracking tools or look over your budget once a week to find places where you can save money. It takes time to change how you spend money, but if you stick with it, you can get your budget back to the right percentages.

What is Q4? Can I change the percentages if my income goes up or down?

Yes, the rule can be changed. A lot of people change the traditional 50/30/20 split to fit their current financial situation better. If your basic costs go above 50% for a short time, you might want to change the percentages (for example, to 60/20/20) until things settle down. The main goal is to keep a balance that will help your finances stay healthy in the long run.

Q5. How can I best keep track of my progress on this rule?

Using a budgeting tool, like an app like YNAB or Mint, a spreadsheet, or even a notebook, is the best way to go. Weekly reviews and monthly audits are examples of regular check-ins that help you keep track of how much you spend in each category. You can also set up automatic transfers for savings and paying off debt to help you stay on track even when you’re busy.

More frequently asked questions:

- Should I include costs that aren’t regular? Yes. To prepare for these costs, set up sinking funds or spread out your annual costs over your monthly budget.

- How can I stay motivated when things are hard? Celebrate small wins and keep in mind that even slow progress can lead to habits that last.

- Can the rule help me get a better credit score? The rule helps improve your credit score over time by lowering your debt and encouraging you to make regular payments.

Last Thoughts

The 50/30/20 budgeting rule is more than just a formula; it can help you make big changes in your finances. The stories shared here show how people have been able to achieve so much by simply following a structured but flexible plan. They range from paying off credit card debt to building strong emergency funds, saving for a home, managing variable freelance income, and getting used to retirement.

These real-life examples show that change is possible no matter where you are in your financial journey. You can take back control of your money and make a future without money stress if you are disciplined, flexible, and get some help from technology. Begin with small steps, keep track of how you’re doing, and stay focused on your goals. Your story about how you did well with your budget is waiting to be written.

Begin Today:

Choose a day, make a budget using the 50/30/20 rule, and stick to it for 30 days. Every little thing you do adds up, and soon you’ll be on your way to being free from money.

Good luck with your budget!